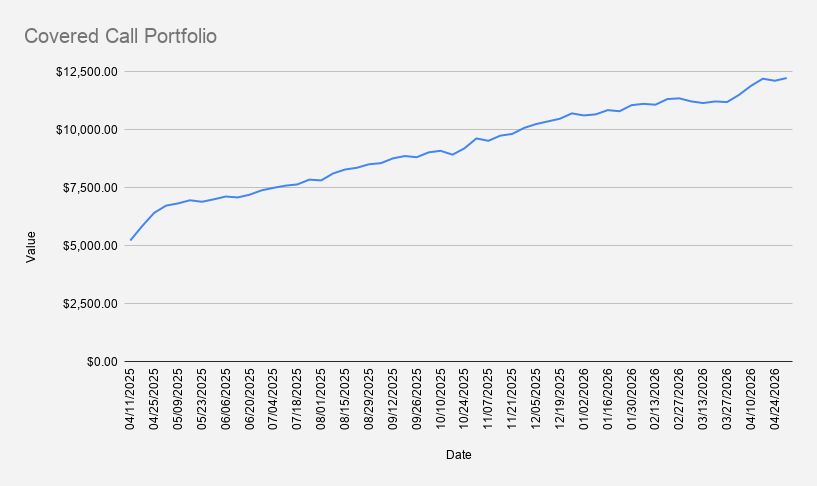

As of May 1st 2026, our options trading driven stock portfolio increased slightly by +0.97%, closing at $12,218.

This week was one of the rare times I didn’t mind seeing NVDA drop—from $210 to below $200. As a put seller, sharp rallies are actually uncomfortable: premiums compress, entries get worse, and the risk of a sudden pullback increases. That’s exactly what played out—after a strong run, the stock finally pulled back, which is the kind of move I’m positioned for.

On a year-to-date basis, the portfolio is up 15.48%, outperforming both the S&P 500 (+5.71%) and NVDA (+5.87%).

Current options positions:

- NVDA May 8, 2026 187.5/177.5 Bull Put Credit Spread

- 2x BMY Jun 18, 2026 50/46 Bull Put Credit Spread

- PFE May 15, 2026 25 Cash-Secured Put

- DBK FRA JUN 19, 2026 24/20 Bull Put Credit Spread

- NVDA Nov 20, 2026 $120 Covered Call

Using premium collected from NVDA credit spreads, we added another 0.1 shares of NVDA. The approach remains consistent: use options income not just for cash flow, but to steadily compound the underlying position. Already holding 102.1 NVDA shares.

A key objective of this covered call portfolio is to gradually reduce margin debt while maintaining a core holding of 100 NVDA shares. This week, we generated $58 in options premium.

At the current pace, it would take roughly 58 weeks to eliminate the existing margin debt of -$3,357. That makes it increasingly clear that, at this rate, bringing the margin balance to zero within 2026 is unlikely. Given the current risk exposure, I’m comfortable extending that timeline into 2027, though even that isn’t guaranteed.

During the week, I was tempted to open additional positions to push weekly options income toward $100. However, that would have added unnecessary risk. With several spontaneous trades already on the books, increasing exposure further would simply raise tail risk. I held back and avoided adding new positions.

It’s also worth noting that the portfolio is currently generating about one-third to one-half of what it did a year ago. That’s likely a positive development, reflecting more controlled risk. This week’s return on capital was 0.47%—solid by most standards, even if it falls short of the 1% weekly target I aimed for last year.

Looking ahead, I’ll be closely watching next week’s NVDA $187.5/$177.5 put spread into expiry. It’s also time to make a decision on the PFE position expiring May 15—whether to keep it on the books or pause it for a while.

If any position comes under pressure, the plan remains to roll forward, ideally for a net credit.

If you enjoy our weekly options trading articles, consider subscribing to the newsletter.