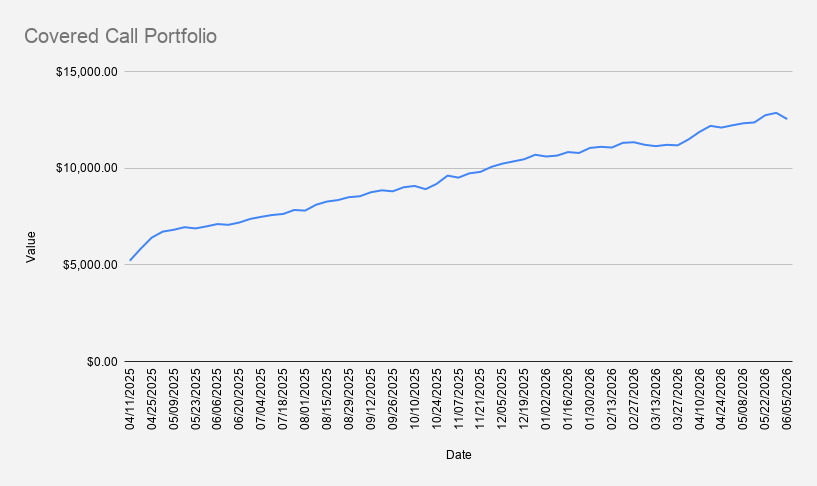

Portfolio Value: $12,540

Weekly Change: -2.5%

YTD Return: +21.07%

Options Premium Collected: $157

On June 6, 2026, the portfolio value declined by 2.5% compared to the previous week, finishing at $12,540.

The decline was not caused entirely by stock performance. Currency movements also had an impact. The U.S. dollar strengthened against the euro, with EUR/USD moving toward 1.15. Because part of the portfolio consists of euro-denominated assets, exchange rate fluctuations affect the reported portfolio value even when the underlying positions remain largely unchanged.

Despite this week's decline, the portfolio remains up 21.07% year to date, outperforming both the S&P 500 (+9.21%) and NVIDIA (+19.32%) over the same period.

NFLX Credit Spread Required an Adjustment

The most significant development this week involved my Netflix position.

The original plan was to generate weekly income using bull put credit spreads on two core holdings: NVIDIA and Netflix. The idea was to diversify premium income instead of relying on a single underlying stock.

In practice, the Netflix position came under pressure almost immediately.

I initially rolled the bull put spread to a later expiration. As Netflix continued moving lower, I decided to make a larger adjustment by converting the position into a cash-secured put expiring in August with a $76 strike price while collecting additional premium.

This serves as a reminder that even relatively conservative option strategies can require adjustments when the underlying stock experiences a sharp move.

For now, NVIDIA remains my primary candidate for weekly credit spreads, while Netflix has shifted into a longer-term cash-secured put position.

Adding Lufthansa With a Cash-Secured Put

I also opened a new position in Lufthansa this week.

After booking a trip to Ireland with Lufthansa, I decided to take a closer look at the company and sold a cash-secured put on Lufthansa shares traded on the Frankfurt Stock Exchange.

The position is:

LHA FRA Sep 18, 2026 7.6 Cash-Secured Put

Unlike my weekly income trades, this is a longer-dated position that fits into the portfolio's European equity allocation.

Current Options Positions

- NVDA Jun 12, 2026 197.5/185 Bull Put Credit Spread

- 2× BMY Jun 18, 2026 50/46 Bull Put Credit Spread

- DBK FRA Jun 19, 2026 24/20 Bull Put Credit Spread (EUR)

- NFLX Aug 21, 2026 76 Cash-Secured Put

- LHA FRA Sep 18, 2026 7.6 Cash-Secured Put (EUR)

- ARCC Sep 18, 2026 16 Cash-Secured Put

- NVDA Jun 17, 2027 $125 Covered Call

Most short-term premium continues to come from credit spreads, particularly on NVIDIA. Longer-dated positions such as NFLX, Lufthansa, and ARCC now function primarily as income-generating cash-secured puts.

Reinvesting Premium Into Shares

Premium collected this week was reinvested into additional shares:

- 0.1 shares of NVDA

- 0.1 shares of NFLX

One of the main goals of this portfolio is to use options income not only to generate cash flow but also to gradually increase ownership in quality companies. Even relatively small weekly purchases can compound over time.

I view the portfolio as both an income portfolio and a long-term growth portfolio. Rather than simply collecting premium, the objective is to steadily build ownership through consistent reinvestment.

$157 in Options Premium

During the week, the portfolio generated $157 in options premium.

A significant portion of that income came from adjusting the Netflix position and opening the Lufthansa cash-secured put.

I do not expect this level of premium every week. With the current portfolio size and prevailing market conditions, consistently generating more than $100 per week would likely require accepting additional risk, which is not currently my objective.

Margin Debt Below $3,000

One encouraging milestone this week was the continued reduction of margin debt.

For the first time since starting this portfolio, the margin balance fell below $3,000, reaching approximately -$2,967.

At this week's premium level, the remaining balance could theoretically be eliminated within about 19 weeks. However, that assumes unusually favorable market conditions and should not be considered a realistic expectation.

A dividend payment from Deutsche Bank also contributed to lowering the margin balance.

My focus remains on steadily reducing leverage while maintaining disciplined risk management rather than trying to eliminate margin as quickly as possible.

Position to Watch Next Week

The key position heading into next week is:

- NVDA 197.5/185 Bull Put Credit Spread

If the position comes under pressure, the plan remains unchanged: continue managing the trade by rolling forward when appropriate while prioritizing long-term portfolio stability.

Final Thoughts

This week demonstrated that even well-planned strategies sometimes require adjustments. The Netflix credit spread evolved into a longer-term cash-secured put, while the portfolio still generated $157 in premium, reduced margin debt below $3,000, and added additional shares of NVIDIA and Netflix.

The long-term objective remains unchanged: combine options income, dividends, covered calls, cash-secured puts, and disciplined reinvestment to steadily grow both portfolio value and future income.

Disclaimer: This trade journal reflects my personal portfolio activity and is shared for educational and informational purposes only. Nothing in this article should be considered investment advice or a recommendation to buy or sell any security or financial instrument. Options trading involves risk and may not be suitable for all investors.