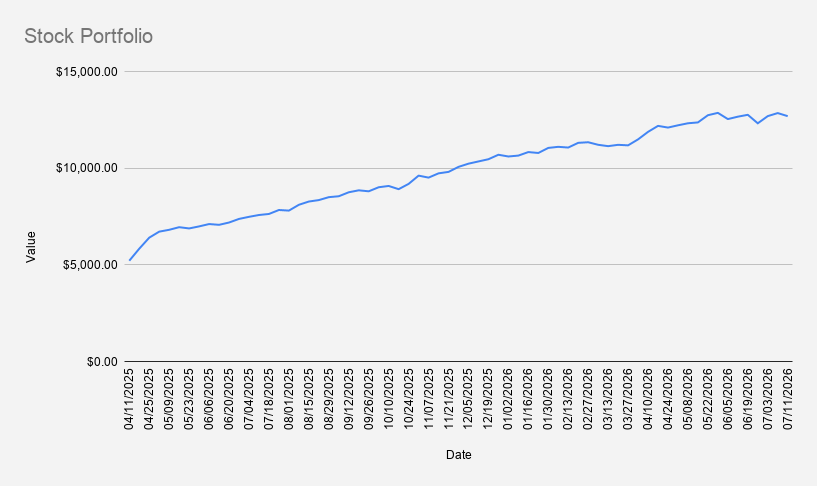

As of July 17, 2026, our stock portfolio closed at $12,691, loosing -1.24% week over week.

The loss came after Netflix’s earnings report, which sent NFLX shares down roughly 10% at one point. Although we hold only a small position in the stock itself, our longer-dated NFLX put option created a meaningful drag on the overall portfolio.

Had NFLX remained flat or reacted positively to the earnings report, the portfolio likely would have crossed the $13,000 mark for the first time. That remains an important milestone—and something to keep working toward.

I originally opened the trade as a supplement to our weekly options income, but it has been problematic for the past few months—almost from the moment it was initiated in May.

That is part of options trading and risk management. Sharp moves like this are especially noticeable in smaller portfolios such as the one I manage.

I may have panicked slightly, but I decided to roll the position forward and down. Fortunately, the adjustment was completed for a net credit, providing a much-needed boost to this week’s total options premium.

Hopefully, I will not regret that decision a few months from now.

On a year-to-date basis, the portfolio is up 24.22%, outperforming both the S&P 500 (+8.88%) and NVIDIA (+13.91%). It is also worth noting that NFLX is now down 25.04%.

Current Options Positions

- NVDA Jul 24, 2026 192.5/182.5 Bull Put Credit Spread

- LHA FRA Sep 18, 2026 7.6 Cash-Secured Put (EUR)

- ARCC Sep 18, 2026 16 Cash-Secured Put

- HEL STERV SEP 18, 2026 8.5 Cash-Secured Put (EUR)

- NVDA Jun 17, 2027 $125 Covered Call

- NFLX Dec 17, 2027 64 Cash-Secured Put

After our NVDA credit spread expired worthless, I opened a new one.

Our BAC position also expired worthless. However, given the challenges with the NFLX trade and the difficulty of finding attractive premiums in weekly BAC options, I decided to pause trading BAC for the time being.

I also rolled the NFLX $66 put from the June 2027 expiration to the December 2027 expiration and lowered the strike price to $64.

Total options premium collected this week reached $147.60, which is close to ideal. However, nearly half of that amount came from rolling the NFLX position, so generating another $50–$60 in weekly options premium may be challenging over the next few weeks.

Part of the premium income was reinvested into the portfolio by purchasing 0.1 share of NVDA and 0.1 share of NFLX.

The current margin balance decreased to -$2,647, it would theoretically take about 19 weeks to eliminate the debt at this pace.

Realistically, however, I do not expect to continue generating $50+ in weekly premium over the coming months.

My expectation is that weekly options income may average closer to $30–$40, meaning it could take considerably longer to eliminate the remaining margin debt without selling any core stock holdings.

Looking ahead to next week, I will be closely monitoring the NVDA $192.5/182.5 put spread. Should any of our positions come under pressure, the plan is to roll them forward—ideally for a credit.

Never miss an update! Get weekly insights delivered to your inbox—subscribe to the Covered Calls with Reinis Fischer newsletter