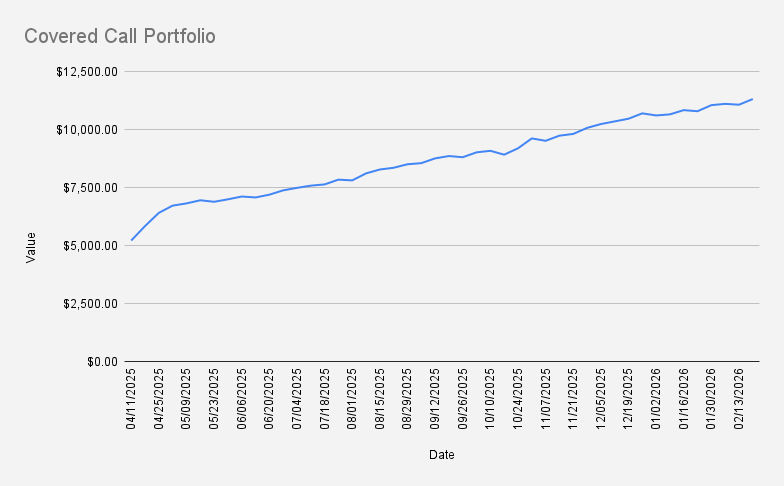

Portfolio Value: $11,312

Weekly Change: +2.20%

YTD Return: +6.91%

Options Premium Collected: $21.90

As of February 20, 2026, the portfolio gained 2.20%, closing the week at $11,312.

Trading activity was relatively quiet this week, but the portfolio continued to make steady progress. While much of my attention was focused on NVIDIA ahead of earnings, the position that ultimately required action was Pfizer (PFE).

That is often how options trading works. The positions you expect to demand attention can behave exactly as planned, while seemingly quiet trades require adjustments.

Adding More McDonald's Shares

Early in the week, I added another 0.1 shares of McDonald's (MCD) to the portfolio.

Over the past few years, I've developed a simple investing habit. Whenever my family visits McDonald's, I occasionally purchase a small amount of MCD stock.

The objective isn't to build a large position quickly. Instead, it serves as a practical way to teach my daughter about investing, business ownership, and how publicly traded companies create value over time.

Current Options Positions

- NVDA Feb 27, 2026 170/150 Bull Put Credit Spread

- 2× BMY Mar 20, 2026 50/46 Bull Put Credit Spread

- PFE Mar 13, 2026 26 Cash-Secured Put

- NVDA Jun 18, 2026 $116 Covered Call

The portfolio continues to rely primarily on three options strategies:

- Bull Put Credit Spreads

- Cash-Secured Puts

- Covered Calls

Rolling the Pfizer Position

The primary adjustment this week involved Pfizer. As the stock approached my short strike, I decided to manage the position proactively instead of waiting until expiration.

The original position was a 26.5/25 Bull Put Credit Spread.

Rather than continuing to manage the spread, I converted the trade into a 26-strike Cash-Secured Put.

The adjustment generated enough additional premium to purchase another 0.5 shares of PFE, bringing my total Pfizer position to approximately one full share.

This reflects one of the core principles of the portfolio: using options premium not only as income but also to gradually increase ownership in productive businesses.

Flexibility Versus Risk

Converting a credit spread into a cash-secured put comes with trade-offs.

Removing the long protective put increases downside exposure, but it also provides greater flexibility for future adjustments and often increases the probability of successfully managing the position over time.

If Pfizer continues trading below $26, additional adjustments may become necessary.

For smaller portfolios, I generally continue to prefer defined-risk credit spreads whenever practical because they provide better capital efficiency and clearly defined maximum risk.

Preparing for NVIDIA Earnings

The biggest upcoming event was NVIDIA's earnings announcement. At the time of writing, the report had not yet been released, leaving a high degree of uncertainty.

Experience has taught me that earnings reactions are difficult to predict. A company can report excellent results and still decline, while disappointing numbers can sometimes be followed by a rally.

Because of that uncertainty, risk management remains more important than trying to forecast short-term price movements.

Weekly Options Income

This week's options activity generated approximately $21.90 in premium.

While this was below some of the stronger premium weeks earlier in the year, I consider that perfectly acceptable.

Not every week offers attractive opportunities. Sometimes the best decision is to preserve capital and avoid unnecessary trades instead of forcing additional premium generation.

Margin Debt Update

One of the long-term objectives of this portfolio remains reducing margin debt while maintaining ownership of at least 100 NVIDIA shares.

At the end of the week, margin debt stood at approximately -$3,943.

Although this week's premium alone would reduce that balance only gradually, premium income naturally varies from week to week depending on available opportunities.

My long-term priorities remain consistent:

- Generate recurring options income.

- Gradually reduce leverage.

- Maintain core long-term holdings.

- Avoid unnecessary risk.

Looking Ahead

The primary positions to monitor next week are:

- NVDA Feb 27, 2026 170/150 Bull Put Credit Spread

- PFE Mar 13, 2026 26 Cash-Secured Put

If either position comes under pressure, my approach remains unchanged:

- Roll positions forward when appropriate.

- Prefer adjustments that collect additional premium.

- Prioritize long-term portfolio stability over short-term results.

Key Takeaway

This week demonstrated that steady progress does not always require exciting trades.

The Pfizer adjustment strengthened the position, additional shares were accumulated, and the portfolio continued moving forward despite generating relatively modest premium.

Some weeks produce substantial options income. Other weeks are primarily about disciplined risk management and patiently building the portfolio one step at a time.

Disclaimer

This trade journal reflects my personal portfolio activity and is shared for educational and informational purposes only. Nothing in this article should be considered investment advice or a recommendation to buy or sell any security, option, or other financial instrument. Options trading involves substantial risk and may not be suitable for all investors. Past performance does not guarantee future results.