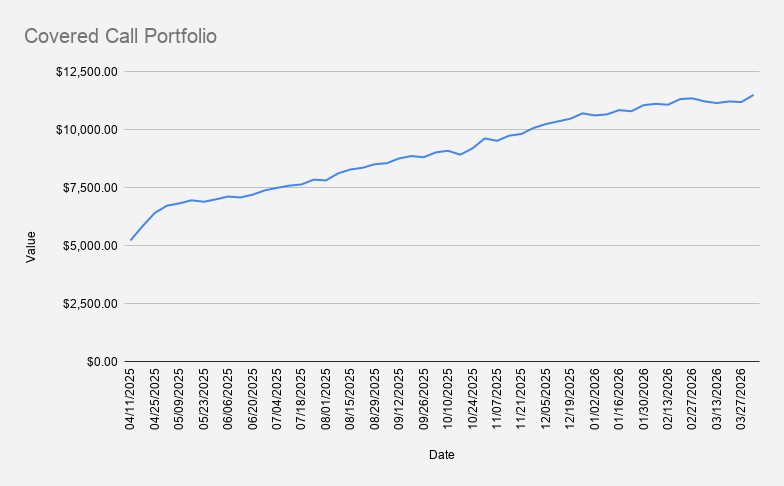

As of April 3, 2026, our options trading driven stock portfolio increased by +2.76%, closing at $11,491.

The week was shortened ahead of Easter, and market sentiment was notably influenced by developments related to the Iran conflict, which has been driving volatility through energy shocks and broader macro uncertainty. Also, as the portfolio is denominated in EUR, it briefly exceeded the €10,000 level several times during the week but ultimately closed below that threshold.

NVDA reclaiming the $170 level supported the overall portfolio. I also resumed the monthly dividend income reports and published the March update.

Given the portfolio’s small size and heavy concentration in NVDA and a few other tech names, dividend income remains limited and non-traditional. During the week, I considered boosting it by adding energy stocks, purely financed from weekly options income, but ultimately decided against expanding into new tickers.

Instead, I’m focusing on existing positions and gradually building a position in PFE through dollar-cost averaging—adding roughly 0.5 shares at a time until reaching at least 10 shares. It’s a modest target, but realistic and directionally meaningful.

On a year-to-date basis, the portfolio is up 11.44%, outperforming both the S&P 500 (-4.16%) and NVDA (-6.74%).

Current options positions:

- NVDA Apr 10, 2026 165/157.5 Bull Put Credit Spread

- 2x BMY Jun 18, 2026 50/46 Bull Put Credit Spread

- PFE May 15, 2026 25 Cash-Secured Put

- NVDA Nov 20, 2026 $120 Covered Call

Using premium collected from NVDA credit spreads, we added another 0.1 shares of NVDA and 0.5 PFE shares The approach remains consistent: use options income not just for cash flow, but to steadily compound the underlying position.

A key objective of this covered call portfolio is to gradually reduce margin debt while maintaining a core holding of 100 NVDA shares. This week, we generated $68 in options premium.

If we can maintain a similar pace, it would take roughly 52 weeks to eliminate the current margin debt of -$3,474.

The goal is straightforward: reduce and ideally eliminate this margin debt during 2026 without selling core positions.

Looking ahead, I’ll be closely watching the NVDA $165/157.5 put spread. If any position comes under pressure, the plan is to roll forward, preferably for a net credit.

I’m also opening a limited number of private coaching sessions. If you want hands-on guidance with covered calls, cash-secured puts, dividend income or navigating the stock market, you can book a session.

Alternatively, join the newsletter to follow the strategy, trades, and ongoing insights.