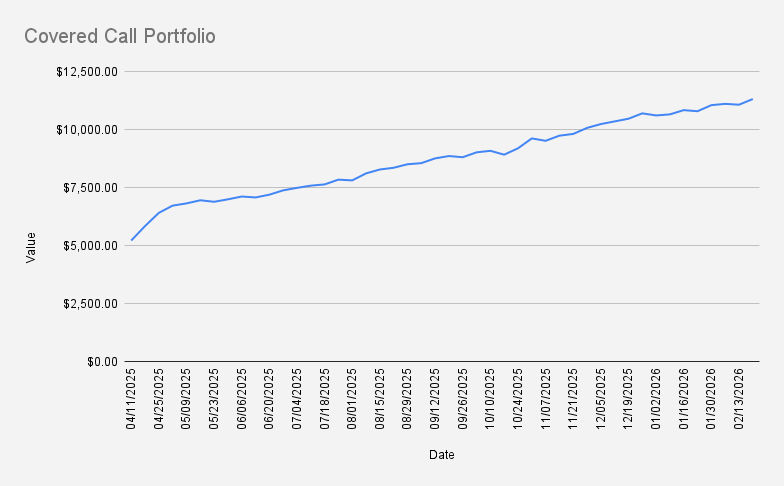

As of February 20, 2026, our covered-call stock portfolio has increased by +2.20% and closed at $11,312.

Growth remained intact, even after rolling PFE forward and down.

For most of the week, my focus was on NVDA, but in the end I had to adjust PFE instead — rolling it forward and lower. That’s part of the process.

NVDA earnings are still ahead next week, so there’s no certainty yet. That said, I’m about 85% confident we’re heading into a strong week.

At the start of the week, we also added 0.1 MCD to the portfolio. That partly explains the slightly higher negative cash balance compared to prior weeks.

We’ve made it a habit to buy a small amount of MCD each time we visit McDonald’s. Not the healthiest routine, but it serves a useful purpose — consistent investing and a practical way to teach my daughter how the stock market works.

Our covered call portfolio is up 6.91% YTD, slightly outperforming the S&P 500 (+0.64%) and NVDA (+0.5%) YTD.

Current options positions:

- NVDA Feb 27, 2026 170/150 Bull Put Credit Spread

- 2X BMY MAR 20, 2026 50/46 Bull Put Credit spread

- PFE MAR 13, 2026 26 Cash-Secured Put

- NVDA JUNE 18, 2026 $116 Covered Call

As noted above, the PFE position came under pressure on Friday. I adjusted the 26.5/25 bull put credit spread into a naked 26 put, collecting enough additional premium to purchase another 0.5 PFE shares. That brings our total dividend position to 1 full PFE share.

This adjustment increases tail risk. If PFE trades below 26 - which remains a meaningful probability - we’ll likely need to roll the position further.

With PFE trading around 26.56 and holding above both its 50- and 200-day moving averages, the technical structure looks more constructive in the short term; however, with the 26 strike sitting just below current price and roughly three weeks until the March 13 expiry, the probability of the stock drifting back toward 26 remains meaningful — likely in the 35–40% range — meaning the chance of testing or even finishing near that level is still relatively high.

One of the primary goals of our covered call stock portfolio is to gradually reduce debt while maintaining a long position of 100 shares in NVDA. Notably, we earned $21 in options premium this week. If we can consistently average that amount, it would take approximately 187 weeks to fully eliminate our margin debt of $3,943. I’d be quite happy to eliminate this margin debt in 2026 without selling any stock - let’s see how it goes.

Looking ahead to next week (s), I will be closely monitoring the PFE 26 put and NVDA $170/150 put spreads . Should any of our positions come under pressure, the plan is to roll them forward—ideally for a credit.

Never miss an update! Get weekly insights delivered to your inbox—subscribe to the Covered Calls with Reinis Fischer newsletter