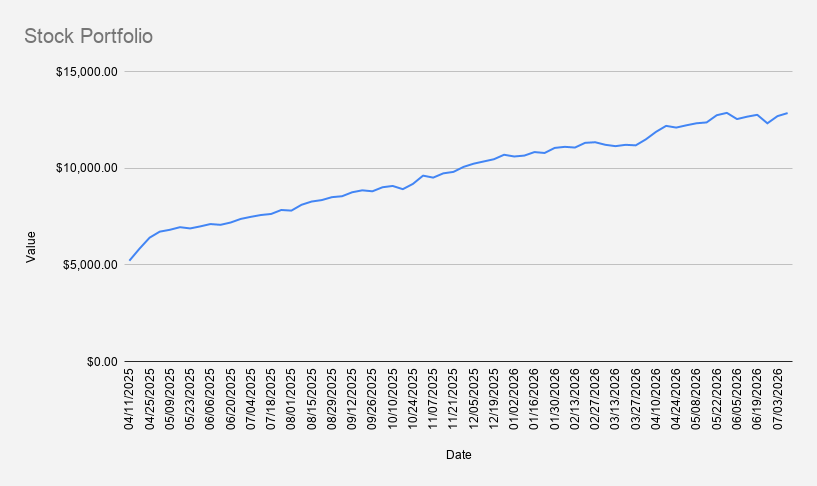

As of July 10, 2026, our dividend stock and options portfolio closed at $12,851, gaining 1.24% week over week.

This week, I opened several new positions, despite saying over the past few weeks that I would probably avoid doing so.

I reintroduced Bank of America stock to both the stock and options sides of the portfolio. Today, I also opened a new cash-secured put position in the Finnish forestry company Stora Enso.

You can read more about my reasoning behind both positions here:

- Why I Bought Bank of America Stock After Selling a Cash-Secured Put

- From Clearing Bushes to Selling Stora Enso Put Options: An 11.65% Annualized Trade

On a year-to-date basis, the portfolio is up 25.79%, outperforming both the S&P 500 (+10.37%) and NVIDIA (+11.24%).

Current Options Positions

- NVDA Jul 17, 2026 195/185 Bull Put Credit Spread

- BAC Jul 17, 2026 56 Cash-Secured Put

- LHA FRA Sep 18, 2026 7.6 Cash-Secured Put (EUR)

- ARCC Sep 18, 2026 16 Cash-Secured Put

- HEL STERV SEP 18, 2026 8.5 Cash-Secured Put (EUR)

- NFLX Jun 17, 2027 66 Cash-Secured Put

- NVDA Jun 17, 2027 $125 Covered Call

After our NVDA credit spread expired worthless, I opened a new one. I also decided to reintroduce a second weekly options position, choosing Bank of America.

However, I have to admit that the portfolio is now entering more dangerous territory. I am already holding an NFLX cash-secured put with a June 2027 expiry, which ties up capital and leaves much less room for error. From here, I need to manage risk very carefully and avoid adding too much exposure.

STERV is the ticker for Stora Enso, a Finnish forestry and renewable materials company. From time to time, I like investing in businesses that I understand, find interesting, or that appeal to me for more personal reasons.

Beyond my interest in the forestry industry, I like this Helsinki-listed stock because it pays a dividend, has listed options, and is denominated in euros. This gives me another way to generate and deploy EUR-denominated cash within my brokerage account.

Total options premium collected this week reached $81, which is slightly better than in recent weeks, when I struggled to generate more than $50–$60. However, it still falls short of my $100 weekly target.

Part of the premium income was reinvested into the portfolio by purchasing 0.1 share of NVDA and 0.1 share of Bank of America.

The current margin balance decreased to -$2,767, it would theoretically take about 35 weeks to eliminate the debt at this pace.

Realistically, however, I do not expect to continue generating $50+ in weekly premium over the coming months.

My expectation is that weekly options income may average closer to $30–$40, meaning it could take considerably longer to eliminate the remaining margin debt without selling any core stock holdings.

However, if the new weekly BAC position performs better than my previous attempt with NFLX, I may be able to generate closer to $40–$50 per week. For now, though, this is only an estimate—not a promise.

Looking ahead to next week, I will be closely monitoring the NVDA $195/185 put spread and BAC 56 put . Should any of our positions come under pressure, the plan is to roll them forward—ideally for a credit.

Never miss an update! Get weekly insights delivered to your inbox—subscribe to the Covered Calls with Reinis Fischer newsletter