Options trades do not always follow the original plan.

In May 2026, I opened a position in Netflix, Inc. (NASDAQ: NFLX) by selling put credit spreads. The initial idea was straightforward: collect option premium while keeping the maximum loss defined through long protective puts.

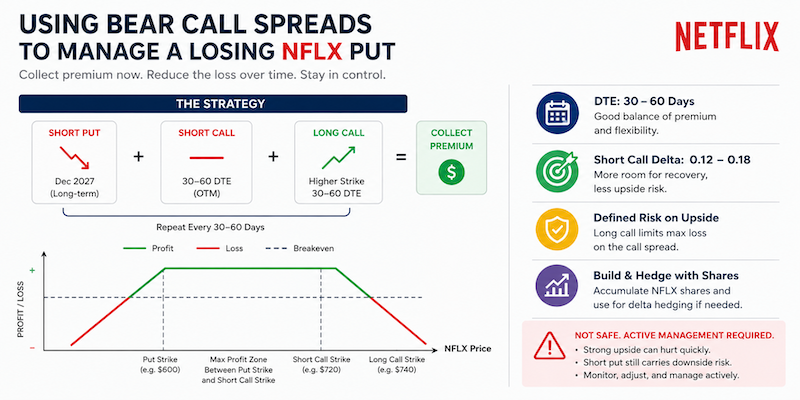

As NFLX weakened and the original spreads came under pressure, I changed the structure. I removed the protective legs and converted the position into what I considered a cash-secured put strategy. That increased the premium collected and gave the trade more time, but it also materially increased the downside exposure.

Following Netflix’s July 2026 earnings report, NFLX shares fell sharply. The stock closed July 17 at approximately $68.95, down 7.26% for the session, according to Netflix’s investor-relations stock quote.

I responded by rolling the short put farther into the future. The position now has a December 2027 expiration—more than 17 months away.

$147.60 in Weekly Options Premium Despite Netflix’s 10% Earnings Drop

That roll reduced the immediate pressure and lowered the strike, but it did not eliminate the underlying loss. It exchanged near-term risk for a longer commitment to NFLX.

I am now considering selling shorter-dated bear call spreads against the long-dated short put. The objective is to collect additional premium and gradually offset part of the loss while waiting for the original thesis to recover.

This can work, but it is not a conventional hedge, and it is certainly not a safe or passive strategy.

The Position I Am Managing

The current structure can be thought of as two separate layers.

The core position is:

- A short NFLX put

- December 2027 expiration

- A willingness—or at least an obligation—to buy 100 NFLX shares at the strike if assigned

The proposed overlay would consist of repeatedly selling bear call spreads with approximately 30–60 days to expiration:

- Sell an out-of-the-money NFLX call

- Buy a higher-strike call with the same expiration

- Collect a net credit

- Close, roll or allow the spread to expire before opening another cycle

The long call limits the theoretical loss of each individual call spread. However, the combined position can still become difficult because the short put and bear call spread do not hedge each other symmetrically.

Why a Bear Call Spread Is Not a True Hedge for a Short Put

A short put is generally a bullish position. It benefits when the stock rises, remains above the strike or at least stops falling.

A bear call spread is bearish to neutral. It benefits when the stock remains below the short-call strike.

Putting them together creates a position that may perform best when NFLX trades inside a broad range:

- Above the short-put danger area

- Below the short-call strike

- With sufficient passage of time for both positions to lose extrinsic value

The call spread can generate income if NFLX remains flat, rises modestly or continues drifting lower. But it does not directly protect the short put from a severe decline.

In fact, selling a call spread adds negative delta to a portfolio that may already become increasingly positive-delta as the short put moves deeper in the money.

Therefore, I would not describe this as hedging the downside of the NFLX put. It is more accurately described as an income overlay intended to reduce the position’s cumulative cost basis.

The distinction matters.

A protective put, put debit spread or short stock position could directly offset downside exposure. A bear call spread primarily earns premium by accepting a new risk: NFLX may recover more quickly than expected.

The Central Thesis

The reasoning behind the trade is that NFLX may require time to rebuild confidence following the earnings decline.

If the stock:

- Stabilizes,

- Trades sideways,

- Recovers gradually, or

- Remains below carefully selected call strikes,

then several rounds of bear call spreads may produce credits that partially offset the loss on the long-dated put.

However, if NFLX stages a strong rebound, the short calls can move in the money rapidly. The call-spread losses could then absorb the premium earned from earlier cycles.

That is the central trade-off:

I am attempting to monetize time and elevated uncertainty, but I am accepting the risk of being wrong about the speed of the recovery.

Netflix held its second-quarter 2026 earnings interview on July 16, and its post-earnings decline illustrates why single-stock options can reprice abruptly around company-specific events.

This approach therefore requires active management. It is not a set-and-forget repair strategy.

Choosing the Short-Call Delta

For this type of recovery overlay, I would generally examine short calls around 0.10 to 0.20 delta.

A possible framework is:

Short-call delta | General character |

|---|---|

0.08–0.12 | Conservative, lower credit, more room for recovery |

0.13–0.17 | Balanced starting range |

0.18–0.25 | More premium, but materially greater upside risk |

Above 0.25 | Aggressive for a stock capable of large earnings-driven moves |

Delta measures how much an option’s theoretical value is expected to change for a one-unit movement in the underlying stock, all else equal. Delta also changes as the stock price, time and implied volatility change, so it should not be treated as a fixed probability or a permanent risk measure.

For my situation, the 0.12–0.18 delta area appears more reasonable than selling calls close to the money.

The purpose is not to maximize the premium from one cycle. It is to create enough distance for NFLX to recover without immediately challenging the short strike.

Selling a 0.25- or 0.30-delta call might generate an attractive-looking credit, but it could turn the position into a constant rolling problem after only a moderate rebound.

Selecting the Long Call

After selecting the short call, I would buy a higher-strike call to cap the maximum spread loss.

There are two common approaches.

Fixed-width spread

For example:

- Sell one call

- Buy another call $5 or $10 above it

This makes the risk straightforward to calculate:

Maximum spread loss = spread width − credit received

A $5-wide spread sold for $0.80 has a theoretical maximum loss of:

$5.00 − $0.80 = $4.20 per share, or $420 per contract

Delta-based long call

Another method is to sell approximately a 0.15-delta call and buy a call around 0.05–0.08 delta.

This may produce irregular spread widths, but it links both strikes to the current volatility surface rather than an arbitrary number of dollars.

I generally prefer a fixed-width structure for smaller portfolios because the maximum risk is easier to understand before opening the trade.

Why I Prefer 30–60 Days to Expiration

I am currently inclined toward bear call spreads with 30–60 days to expiration.

That range offers several advantages:

- Meaningful time value

- Less extreme gamma risk than very short-dated options

- Enough time to adjust the trade before expiration

- More opportunity to choose strikes comfortably above the market

- A reasonable balance between premium collection and flexibility

Gamma describes how quickly delta changes as the stock moves. As expiration approaches, an option’s delta can change much more abruptly, particularly when the stock is near the strike. That makes short-dated spreads more sensitive to sudden price moves and can force faster hedge adjustments.

A seven-day spread may appear attractive because of rapid time decay, but a sharp three-day NFLX rally could overwhelm the collected premium before there is a practical opportunity to respond.

Thirty to sixty days does not remove that risk. It simply provides a wider management window.

My tentative preference would be:

- Open around 40–50 DTE

- Start monitoring closely once the spread reaches approximately 21 DTE

- Avoid holding a challenged spread into its final few days

- Avoid opening a cycle that includes the next earnings announcement unless the higher event risk is intentional

Position Size Is More Important Than Premium

The trade should not be sized according to how much premium I want to recover.

It should be sized according to how much additional loss I can tolerate if NFLX rebounds.

A single listed U.S. equity-option contract ordinarily represents 100 shares.

That creates an important asymmetry in my portfolio.

I may own only a small fractional NFLX position while one short put and one call spread each represent exposure connected to 100 shares. The options exposure can therefore be much larger than the stock position.

This is why I would begin with no more than one narrow call spread for each short put, and potentially less exposure where contract sizing permits.

The goal is not to recover the entire paper loss quickly. Trying to do so would encourage selling strikes too close to the current stock price or using spreads that are too wide.

Building an NFLX Stock Position Along the Way

I am also gradually purchasing NFLX shares.

This serves two purposes.

First, I am building an actual long-term position in a company I may eventually own through put assignment anyway.

Second, the shares provide positive delta that can partially offset the negative delta of a challenged bear call spread.

Suppose I own 20 NFLX shares and my short call becomes in the money. Those 20 shares do not fully cover one short call contract, which represents 100 shares, but they reduce the net amount of uncovered upside exposure.

If the short call were ultimately assigned, the shares could potentially be used to satisfy part of the delivery obligation, while the remaining exposure would still need to be managed through the long call, additional share purchases or closing transactions.

This should not be confused with a fully covered call.

A short call is fully covered only when the trader owns the necessary 100 shares per contract. Holding 10, 20 or 50 shares provides only a partial stock offset.

An American-style short equity option may be assigned before expiration whenever it is exercisable. The precise assignment timing is controlled by the long option holder and processed through the clearing system, not by the option writer.

Therefore, accumulating shares can improve flexibility, but it does not eliminate assignment or spread-management risk.

Using Shares for Dynamic Delta Hedging

If NFLX approaches or moves above my short-call strike, another possible response is to buy shares as a delta hedge.

For example, assume the overall position has a net delta of –25.

That means the portfolio behaves approximately like a short position of 25 NFLX shares for a small movement in the stock, although the relationship changes continuously.

Buying approximately 25 shares would bring the position closer to delta neutral at that moment.

Interactive Brokers describes delta hedging as taking offsetting positions in the underlying and the option to reduce directional risk, and its tools can calculate a stock quantity intended to offset option delta.

But delta hedging is not a one-time solution.

As NFLX rises:

- The short call’s delta becomes more negative

- The long call’s positive delta also increases

- The net spread delta changes

- The short put’s delta changes

- The number of shares required for a neutral hedge changes

This is why dynamic hedging requires repeated decisions.

If I buy shares during a rally and NFLX subsequently falls, those shares can lose value while the call spread improves. I may then need to sell some shares to avoid becoming excessively bullish again.

Delta hedging can reduce immediate directional exposure, but it introduces trading costs, timing risk and the possibility of repeatedly buying high and selling low.

A Possible Management Framework

I am considering the following rule-based structure.

Entry

- Select approximately 30–60 DTE

- Sell a call around 0.12–0.18 delta

- Buy a higher call to define maximum loss

- Avoid using a spread whose maximum loss would materially damage the portfolio

- Prefer expirations that do not include earnings

Profit management

I may close the spread after capturing approximately 40–60% of the initial credit rather than waiting for the final few dollars.

Closing early would release risk and allow me to reassess the NFLX chart, volatility and next expiration independently.

Upside challenge

If NFLX approaches the short strike, I would evaluate:

- Closing the spread for a controlled loss

- Rolling it upward and farther out, preferably for a credit

- Reducing the number of spreads

- Buying shares to offset part of the negative delta

- Allowing the defined-risk spread to reach its predetermined maximum loss

The correct response would depend on the remaining extrinsic value, implied volatility, time to expiration and the state of the long-dated put.

Rolling should not be automatic. A roll is economically a closing trade followed by a new opening trade. It may improve the strike or generate a credit, but it does not erase the loss on the original spread.

Downside continuation

If NFLX declines further, the call spread should become profitable, but the short put may lose substantially more than the spread earns.

That is another reason not to call the bear call spread a complete hedge.

A $50 or $100 call-spread profit is small compared with the potential loss from controlling 100 shares through a deeply in-the-money short put.

Understanding the Combined Delta

The combined trade may contain:

- Positive delta from the short put

- Negative delta from the short-call spread

- Positive delta from NFLX shares

- Changing gamma exposure from all option legs

At first, these positions may appear to offset each other.

But the balance is unstable.

If NFLX falls sharply, the short put may approach a delta near +1.00, meaning it behaves increasingly like 100 long shares. The call spread may lose much of its negative delta because both calls become far out of the money.

If NFLX rallies sharply, the put delta may shrink while the call spread becomes more negatively directional.

The position can therefore change from strongly bullish to approximately neutral or even temporarily bearish as NFLX moves.

This is one reason a multi-leg recovery trade must be monitored as a portfolio, not as several independent trades.

The Main Risks

1. Violent NFLX recovery

A strong recovery is the clearest risk to the call-spread overlay.

NFLX could rebound because of:

- Improved investor sentiment

- Analyst upgrades

- Better engagement data

- Advertising growth

- Transaction-related developments

- A broad technology-sector rally

- Strong future earnings or guidance

The spread’s defined risk prevents unlimited losses, but repeated maximum-loss spreads could meaningfully increase the total damage from the original trade.

2. Further NFLX decline

The call spread may profit, but it does little to protect the short put from a major decline.

The combined position remains exposed to NFLX’s downside.

3. Volatility expansion

An increase in implied volatility can raise the value of both the short put and the short call spread, producing mark-to-market losses even when neither strike has been breached.

4. Early assignment

The short call or short put can theoretically be assigned before expiration. Assignment is especially relevant when an option is deep in the money and has little remaining extrinsic value.

Netflix currently does not pay a regular dividend, so dividend-related early call assignment may be less relevant than it would be for a dividend-paying stock. Nevertheless, assignment remains contractually possible.

5. Margin and liquidity

A broker may change margin requirements as volatility and concentration risk change. Wide bid-ask spreads can also make repeated rolling expensive.

6. Strategy drift

The original trade began as a defined-risk credit spread.

It then became a short put.

It was subsequently extended to December 2027.

Adding bear call spreads and dynamic share hedges makes the position even more complex.

Each modification may be rational on its own, but together they can create a position that no longer resembles the original thesis.

That is the behavioral risk I need to monitor most closely.

What Would Invalidate the Strategy?

I would reconsider the call-spread overlay if:

- My long-term view of Netflix becomes clearly bullish

- NFLX begins a strong technical recovery

- The credits available at conservative deltas become too small

- Bid-ask spreads make adjustments uneconomic

- The total options exposure becomes too large relative to the portfolio

- Repeated spread losses exceed the income generated

- I am unwilling to actively monitor the position

- Buying or holding the stock directly becomes simpler than managing the derivatives structure

The purpose of the overlay is to improve the trade’s economics—not to defend the original decision indefinitely.

Bottom Line

Selling 30–60 DTE NFLX bear call spreads may help me collect incremental premium while managing a December 2027 short put.

The most reasonable starting point appears to be:

- Approximately 0.12–0.18 delta on the short call

- Defined-risk call-spread width

- Modest position sizing

- No intentional earnings exposure

- Active management before expiration

- Gradual accumulation of NFLX shares

- Optional share-based delta hedging if the upside becomes challenging

But this is not free income.

The call spreads do not protect the short put from a severe decline. Instead, they introduce a second risk: NFLX may recover sharply and challenge the short calls.

Accumulating shares can partially offset that upside risk, and dynamic delta hedging can provide additional control. However, both approaches add capital requirements and management complexity.

The strategy may be suitable as a carefully sized recovery overlay, but it is not a safe rescue mechanism. It demands predefined limits, realistic expectations and a willingness to close positions when the underlying assumptions no longer hold.

The objective is not to force the NFLX trade back into profit at any cost.

It is to reduce the damage gradually—without allowing the repair strategy to become more dangerous than the original position.

Disclosure: This article documents my personal trading process and is not financial advice. Options involve substantial risk and are not suitable for every investor. The Options Clearing Corporation recommends reviewing the Characteristics and Risks of Standardized Options before trading listed options.