This week was focused on managing positions after NVDA earnings, collecting another round of options premium, and continuing to grow the underlying stock portfolio.

Nvidia reported strong results, but the market reaction was relatively muted. NVDA pulled back slightly after the announcement, which is often where option sellers can find new opportunities.

Because most of my short-term income comes from bull put spreads and covered calls, a modest decline is not necessarily a negative development. Lower implied volatility after earnings can also benefit existing short-option positions.

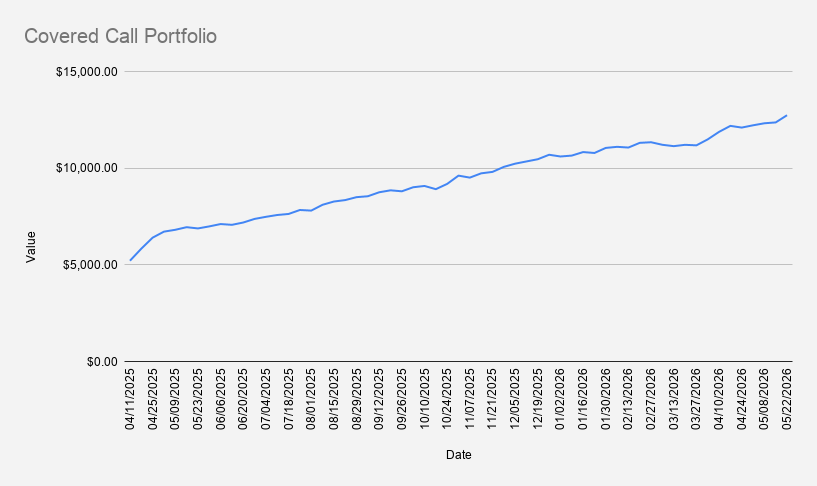

As of May 22, 2026, the portfolio was valued at $12,740, representing a 22.48% gain year to date. For comparison, the S&P 500 had returned approximately 9.26% during the same period, while NVDA was up 15.39%.

Why NVDA Remains My Main Options Income Stock

I continue to concentrate most of my options activity around NVDA for one main reason: liquidity.

As one of the largest publicly traded companies in the world, Nvidia has an exceptionally active options market. High liquidity generally means tighter bid-ask spreads, better fills, and more flexibility when a position needs to be adjusted or rolled.

For an income-focused options portfolio, that is a major advantage.

This week I considered expanding into stocks such as Apple and Palantir, but I ultimately decided against it. At the current portfolio size, I do not see much value in adding more positions simply for the appearance of diversification.

Instead, I prefer to concentrate on a limited number of highly liquid companies that I understand reasonably well.

Adding NFLX to the Options Rotation

One change this week was the addition of NFLX credit spreads.

The intention is not to replace NVDA, but to introduce another liquid underlying capable of generating attractive option premium.

Compared with NVDA, Netflix generally requires me to accept a slightly lower theoretical probability of profit to earn a similar amount of premium. While some NVDA spreads can be structured with probabilities above 90%, NFLX trades often fall into the mid-to-high 80% range.

That remains acceptable to me as long as the position size is conservative and the maximum risk is clearly understood before the trade is opened.

The objective is not to collect the highest possible premium. The objective is to generate repeatable income without allowing one position to create disproportionate portfolio risk.

Current Options Positions

The portfolio currently holds the following options positions:

- NVDA May 29, 2026 205/195 bull put credit spread

- NFLX May 29, 2026 85/80 bull put credit spread

- 2x BMY June 18, 2026 50/46 bull put credit spreads

- DBK FRA June 19, 2026 24/20 bull put credit spread

- ARCC September 18, 2026 $16 cash-secured put

- NVDA June 17, 2027 $125 covered call

All weekly positions from the previous cycle expired worthless, allowing me to keep the full premium and redeploy the available capital into new trades.

That is the preferred outcome with short-duration credit spreads: collect the premium, allow the options to expire, and move on to the next carefully selected opportunity.

Converting Options Premium Into Long-Term Assets

One of the central ideas behind this portfolio is that options income should not simply remain in cash.

I use part of the premium generated from options trades to gradually purchase shares in companies I want to own over the long term.

This week, options premium helped fund the following purchases:

- 0.1 shares of McDonald’s (MCD)

- 0.1 shares of Netflix (NFLX)

- 0.1 shares of Nvidia (NVDA)

- 0.5 shares of Pfizer (PFE)

These purchases may appear insignificant when viewed individually, but they accumulate over time.

The goal is not to make a life-changing stock purchase every week. The goal is to consistently convert short-term premium income into productive long-term assets.

Dividend Income Continues to Grow

The dividend side of the portfolio also moved higher this week.

The latest share purchases increased projected annual dividend income by approximately $1.31.

That is not a dramatic increase on its own, but small additions repeated over many weeks can eventually become meaningful.

Deutsche Bank is also approaching its annual dividend payment. With 26 shares currently held, projected annual dividend income for the portfolio has climbed to approximately $90 per year.

The next milestone is straightforward: increasing annual dividend income beyond $100.

It is still a modest amount, but it represents another step toward building a portfolio capable of generating income independently of new capital contributions.

Weekly Premium Income and Margin Reduction

The options portfolio generated $66.90 in premium income this week.

I would like weekly premium income to exceed $100 more consistently, but I am not willing to take substantially more risk merely to reach an arbitrary target.

The portfolio still carries approximately $3,135 in margin debt, and reducing that balance remains one of my main priorities.

At the current pace, eliminating the debt will take time, and that is acceptable.

I would rather reduce leverage gradually while maintaining disciplined risk than chase higher returns and expose the portfolio to unnecessary drawdowns.

What I Am Watching Next Week

The primary positions on my radar remain:

- NVDA 205/195 bull put credit spread

- NFLX 85/80 bull put credit spread

If either position comes under pressure, my preferred adjustment remains to roll forward when practical, ideally for a net credit and without materially increasing the risk.

One of the advantages of trading highly liquid stocks is that there are usually several adjustment choices available before a position becomes unmanageable.

The objective is not to avoid every losing trade. That is impossible.

The objective is to manage risk well enough that one losing position does not become a portfolio-threatening event.

Portfolio Principles

As the portfolio grows, the underlying philosophy remains unchanged:

- Generate recurring options premium

- Focus on highly liquid stocks

- Use defined-risk strategies whenever practical

- Reinvest premium into long-term holdings

- Increase dividend income gradually

- Reduce margin debt responsibly

- Prioritize capital preservation over maximum returns

A year-to-date return above 22% is encouraging.

However, the long-term objective is not to produce one unusually strong year.

The objective is to build a portfolio that can continue generating income, accumulating quality assets, and compounding capital for many years.

Disclaimer: This article reflects my personal portfolio activity and market observations. It is published for informational and educational purposes only and does not constitute financial, investment, tax, or legal advice.

Options trading involves substantial risk and may not be suitable for all investors. Past performance does not guarantee future results. Always conduct your own research and consult a qualified financial professional before making investment decisions.