The Ultimate NVDA Options Strategy Guide: Cash-Secured Puts, Covered Calls & Credit Spreads

NVIDIA (NASDAQ: NVDA) has become one of the most actively traded stocks in the world. Between the AI boom, extreme volatility, institutional demand, and highly liquid options market, NVDA has evolved into a unique environment for systematic options trading.

This article explains a practical framework for trading NVDA using:

- Cash-secured puts

- Covered calls

- Credit spreads

- Active position management

- Volatility-aware risk control

The goal is not to predict short-term price movements. The goal is to systematically generate premium income while managing downside exposure and surviving high-volatility market conditions.

This framework has been actively used and refined since March–April 2025 across multiple volatility regimes, earnings cycles, and sharp market drawdowns.

Most importantly:

This is not a “safe income strategy.”

Selling options on NVDA carries substantial risk and can produce significant losses when poorly managed or overleveraged.

Understanding those risks is far more important than understanding the premium collected.

Why NVDA Is Attractive for Options Trading

Very few stocks combine all of the following characteristics simultaneously:

- Massive daily volume

- Deep institutional liquidity

- Tight option spreads

- Weekly expirations

- Elevated implied volatility

- Strong long-term narrative momentum

NVDA offers all of them.

For options traders, this creates an unusually efficient premium-selling environment.

Compared to slower-moving large-cap stocks, NVDA options frequently price in substantial expected moves. This allows traders to collect larger premiums relative to deployed capital.

At the same time, the stock can move violently.

A 5–10% move in a single session is entirely possible, especially around:

- earnings

- macroeconomic events

- AI-related headlines

- semiconductor sector rotations

- geopolitical tensions

This combination of:

- high premium

- high liquidity

- high volatility

is precisely what makes NVDA attractive — and dangerous.

Understanding the Core NVDA Options Framework

The strategy framework revolves around three primary structures:

- Cash-secured puts

- Covered calls

- Defined-risk credit spreads

These are not used independently. They function together as part of an actively managed options portfolio.

The framework prioritizes:

- premium generation

- capital efficiency

- rolling mechanics

- controlled assignment

- long-term survivability

not short-term speculation.

Cash-Secured Puts on NVDA

Cash-secured puts are often the foundation of the strategy.

The basic idea is simple:

A trader sells a put option while keeping enough cash available to purchase 100 shares if assigned.

If the option expires worthless:

- the trader keeps the premium.

If assigned:

- the trader acquires NVDA shares at the strike price.

In practice, however, the process is much more complex.

Why Sell Puts on NVDA?

The primary reasons include:

- Elevated option premiums

- Willingness to own shares at lower prices

- Systematic entry into positions

- Income generation during sideways markets

Many traders prefer selling puts instead of placing limit orders because the premium reduces effective cost basis.

Example:

If NVDA trades at $150 and a trader sells a $140 put for $4:

- effective purchase price becomes $136 if assigned.

That sounds attractive.

Until NVDA suddenly trades at $110.

This is where most beginner explanations fail.

The Real Risk of Cash-Secured Puts

The risk is not assignment.

The risk is:

- violent downside acceleration

- volatility expansion

- overleveraging

- oversized position concentration

A trader who continuously sells puts too aggressively during bullish conditions may eventually face:

- multiple assignments

- rapidly expanding unrealized losses

- margin pressure

- forced liquidation

NVDA can remain irrationally volatile far longer than many traders expect.

The premium is compensation for risk — not free income.

Strike Selection and Delta Targeting

Many systematic traders use delta as a probability framework.

Examples:

- 10 delta → lower premium, lower assignment probability

- 30 delta → higher premium, higher assignment probability

Lower delta strikes generally provide:

- more downside cushion

- smaller premiums

- higher probability of expiration worthless

Higher delta strikes provide:

- larger income

- faster theta decay

- greater directional exposure

There is no universally “correct” delta.

Strike selection depends on:

- volatility regime

- market conditions

- portfolio exposure

- willingness to own shares

- macro risk environment

Covered Calls on NVDA

Covered calls are typically used after share assignment or intentional long stock acquisition.

The trader owns NVDA shares and sells call options against them.

The objective:

- generate additional income

- reduce cost basis

- monetize elevated implied volatility

Covered calls appear conservative on paper.

In reality, they involve difficult trade-offs.

The Main Covered Call Problem: Capped Upside

NVDA is capable of explosive upside moves.

Selling covered calls means:

- accepting limited upside participation in exchange for immediate premium.

This creates emotional pressure when the stock rallies sharply through the strike price.

Many traders panic and:

- buy back calls at losses

- chase upside

- abandon systematic management

Covered call management requires accepting that:

- some upside will be sacrificed.

Without that acceptance, the strategy becomes emotionally unstable.

Rolling Covered Calls

Rolling is one of the most important skills in systematic options trading.

A covered call can be:

- rolled higher

- rolled further out in time

- adjusted for additional credit

- repositioned during volatility changes

However, rolling is not magic.

Bad rolls can:

- lock in losses

- increase directional exposure

- reduce flexibility

- create margin stress

A successful long-term framework depends less on individual trades and more on disciplined adjustment mechanics over hundreds of occurrences.

Credit Spreads on NVDA

Credit spreads introduce defined-risk structures.

Common examples:

- put credit spreads

- call credit spreads

These strategies:

- reduce collateral requirements

- cap maximum losses

- improve capital efficiency

Example:

A trader may:

- sell a $140 put

- buy a $130 put

This creates a bullish put credit spread.

Maximum profit:

- premium received

Maximum loss:

- spread width minus premium

Defined risk sounds safer.

But spreads introduce their own challenges.

The Hidden Danger of Credit Spreads

Spreads can fail extremely quickly during violent directional moves.

Especially near expiration:

- gamma accelerates

- spread values expand rapidly

- liquidity can deteriorate

- adjustment flexibility shrinks

Many traders underestimate:

- assignment complications

- pin risk

- expiration-week volatility

- fast-moving losses

Defined risk does not mean low risk.

It simply means losses are capped mathematically.

Trade Adjustments and Position Management

One of the most overlooked aspects of trading NVDA options is trade adjustment. Most beginner-focused options content spends almost all its time discussing:

- entries

- strike selection

- premium collection

In reality, long-term success often depends far more on how positions are managed after entry. This is especially true when trading NVDA, where volatility and momentum can change extremely quickly. A profitable options framework is not static. It requires continuous decision-making based on:

- stock price movement

- time remaining until expiration

- implied volatility

- portfolio exposure

- overall market conditions

Trade adjustments therefore become a core part of systematic NVDA options trading.

Different Approaches to Trade Adjustments

There is no single universally correct way to adjust options positions. Some traders use:

- delta-based adjustments

- volatility-based adjustments

- time-to-expiration rules

- technical analysis

- price-based management

In practice, many experienced traders combine multiple methods simultaneously.

Delta-Based Adjustments

Delta-based management involves adjusting positions once option delta reaches a predefined threshold. For example:

- rolling a short put spread once delta expands beyond 0.30 or 0.40

- reducing directional exposure as assignment probability increases

This approach is popular because delta acts as a rough probability model. However, in highly volatile stocks like NVDA, delta can expand extremely quickly during sharp market moves.

Volatility-Based Adjustments

Some traders primarily manage positions based on implied volatility changes. Examples include:

- reducing exposure during volatility spikes

- avoiding aggressive short premium exposure into unstable macro environments

- rolling positions when implied volatility rapidly expands

This becomes particularly important around:

- earnings

- Federal Reserve meetings

- semiconductor sector volatility

- broader market selloffs

In NVDA, volatility itself often becomes one of the largest sources of risk.

Price-Based Adjustments

Personally, I frequently use price-based adjustments alongside broader portfolio considerations. This means I often react to:

- key stock price levels

- momentum shifts

- proximity to short strikes

- market structure changes

rather than relying exclusively on delta thresholds. In practice, this usually leads to earlier adjustments, especially when managing weekly credit spreads. The objective is not maximizing every last dollar of premium. The objective is reducing the probability of allowing a manageable position to become a difficult position.

Why Early Adjustments Matter

One of the biggest mistakes newer options traders make is waiting too long to adjust trades. This is particularly dangerous with short-dated weekly spreads. As expiration approaches:

- gamma risk accelerates

- small stock moves create larger option price swings

- rolling flexibility decreases

- emotional pressure increases

Many traders incorrectly assume:

“The strike is still out of the money, so the trade is safe.”

But options risk is dynamic. A spread that appears manageable on Monday can become highly stressed by Thursday afternoon.

Early adjustments often provide:

- more flexibility

- better liquidity

- improved strike selection

- additional premium opportunities

- reduced probability of large losses

In many cases, proactive management matters more than the original trade entry.

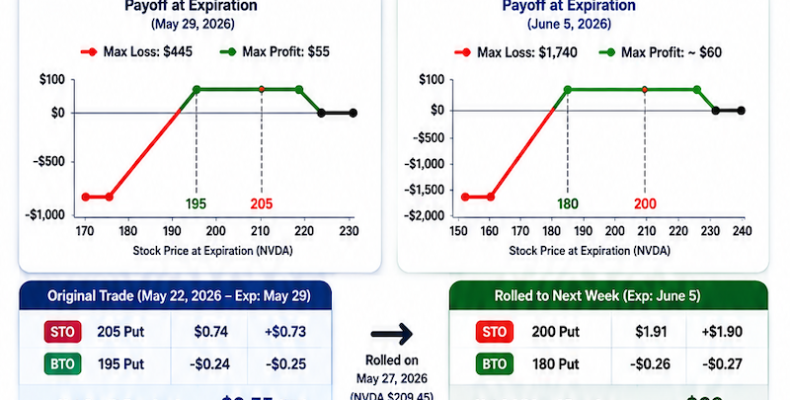

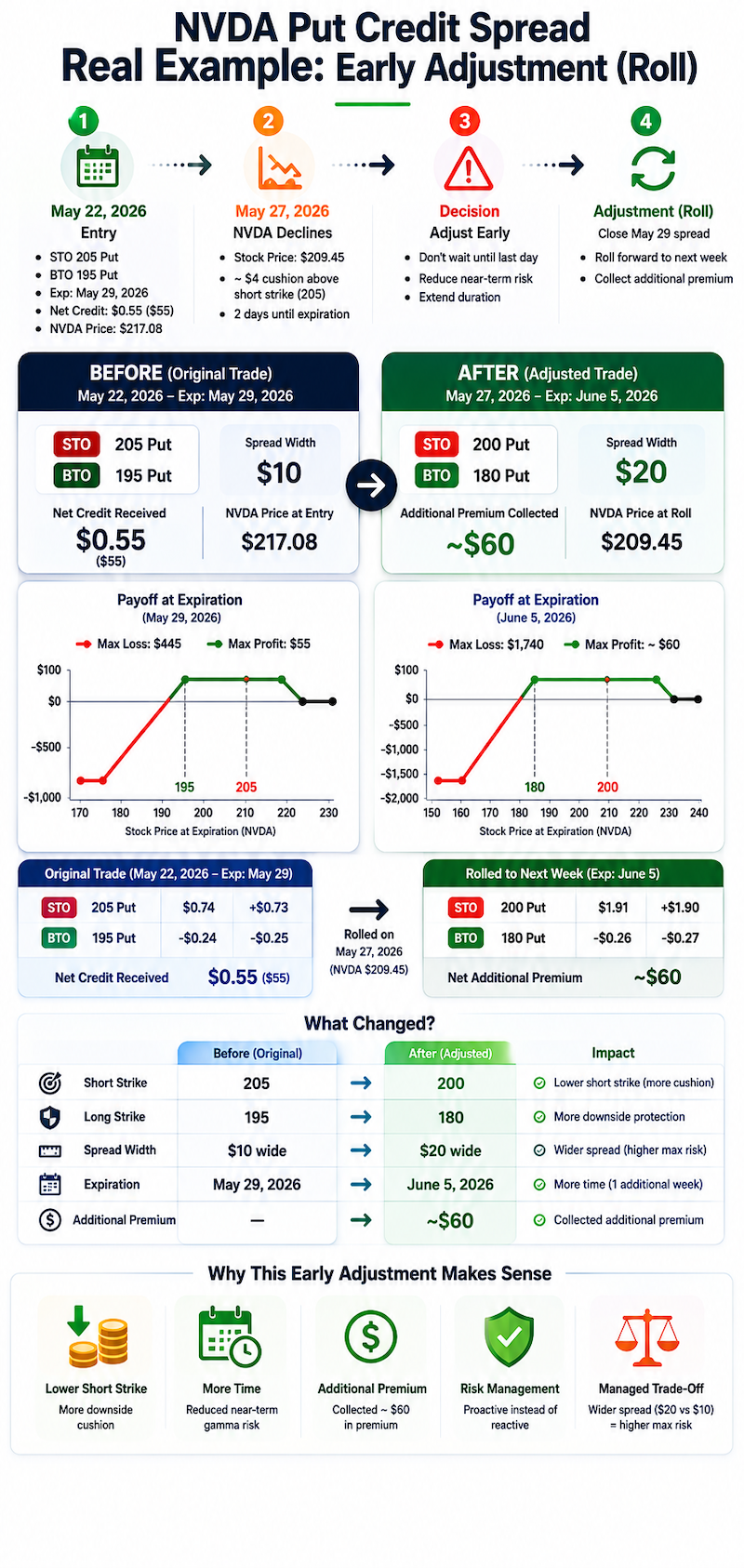

Real Example: Rolling an NVDA Weekly Credit Spread

On May 22, 2026, I opened a weekly NVDA put credit spread using the following structure:

- Sell to Open (STO) 205 Put — Expiration: May 29, 2026

- Buy to Open (BTO) 195 Put — Expiration: May 29, 2026

At the time of entry:

- NVDA stock price: $217.08

- Net credit received: approximately $0.55 ($55 before commissions)

- Spread width: $10

The original thesis was straightforward:

- maintain downside cushion below current price

- benefit from time decay

- allow the spread to expire worthless if NVDA remained stable or bullish

A few trading days later, on May 27, 2026, NVDA had declined to approximately $209.45. Technically, the short 205 strike still remained out of the money, leaving roughly $4 of price cushion above the short strike. Many traders would simply continue holding the position and hope for expiration. Instead, I decided to adjust the trade early.

Why I Rolled the Position Early

Although the spread was still technically safe, several risk factors had changed:

- only two trading days remained until expiration

- downside momentum had accelerated

- gamma exposure increases sharply near expiration

- small stock movements can rapidly expand spread value

- rolling flexibility decreases late in the expiration cycle

Rather than waiting for the position to become stressed, I chose to proactively reduce near-term risk.

The Adjustment

On May 27, 2026, I closed the original May 29 spread:

- Bought back the short 205 put

- Sold the long 195 put

I then rolled the trade forward to the following week by opening a new spread expiring June 5, 2026:

- Sell to Open (STO) 200 Put

- Buy to Open (BTO) 180 Put

This adjustment accomplished several objectives simultaneously:

| Adjustment Component | Before | After |

|---|---|---|

| Short Strike | 205 | 200 |

| Long Strike | 195 | 180 |

| Spread Width | $10 | $20 |

| Expiration | May 29 | June 5 |

| Additional Premium Collected | — | ~$60 |

| NVDA Stock Price | $217.08 at entry | ~$209.45 during adjustment |

What Improved — and What Increased

The adjustment improved the position in several important ways:

Lower Short Strike

Reducing the short strike from 205 to 200 increased downside cushion and improved probability of success.

More Time

Rolling from the current week into the following week reduced immediate expiration pressure and near-term gamma risk.

Additional Premium

The roll generated approximately $60 in additional premium, improving total collected credit.

The Trade-Off: Wider Risk Structure

The adjustment also introduced an important trade-off.

The spread width increased:

- from $10 wide

- to $20 wide

This increased maximum theoretical risk exposure. This is an important reminder.Trade adjustments are not magic. In many cases, adjustments involve exchanging one type of risk for another type of risk

In this example, I accepted wider spread risk in exchange for:

- lower short strike exposure

- more time

- improved positioning

- additional premium collection

That trade-off made sense within the broader portfolio context and market conditions at the time.

Why This Matters for NVDA Options Trading

Many retail traders approach weekly credit spreads passively:

- enter the trade

- wait until expiration

- hope the stock stays above the strike

In highly volatile stocks like NVDA, this approach can become dangerous very quickly.

Systematic trade management often means:

- adjusting early

- accepting smaller losses or reduced profit

- improving probabilities before positions become stressed

Over time, proactive adjustment discipline can become one of the largest differences between:

- controlled risk management

and - reactive emotional trading.

Portfolio Construction Matters More Than Trade Selection

This is one of the most overlooked concepts in retail options trading.

A strategy does not fail because of one bad trade.

It fails because of:

- poor sizing

- excessive leverage

- concentration risk

- correlated exposure

Proper portfolio construction may include:

- staggered expirations

- diversified strike placement

- partial cash reserves

- reduced exposure during earnings

- avoiding full collateral deployment

Many traders destroy otherwise profitable systems simply by allocating too aggressively.

Volatility Is the Entire Game

Most new traders focus on direction.

Professional options management focuses on volatility.

Implied volatility affects:

- premium pricing

- rolling opportunities

- option decay

- risk asymmetry

High implied volatility:

- increases premium

- increases danger

Low implied volatility:

- reduces premium

- often reduces margin of safety for sellers

Understanding volatility expansion and contraction is essential for long-term survival.

Earnings Risk and NVDA

NVDA earnings events can produce extreme overnight repricing.

This creates:

- enormous premiums

- enormous uncertainty

Some traders avoid holding short options through earnings entirely.

Others reduce size dramatically.

There is no universal rule.

But treating earnings premium as “easy money” is one of the fastest ways to destroy a premium-selling account.

The Psychological Side of Trading NVDA Options

The emotional component is massive.

NVDA frequently creates:

- FOMO during rallies

- panic during selloffs

- greed during premium spikes

- revenge trading after losses

Systematic trading requires:

- consistency

- position discipline

- predefined risk limits

- emotional detachment

Most retail traders fail not because the strategy is mathematically flawed, but because emotional decision-making overrides process.

Is This Just the Wheel Strategy?

Partially.

The framework overlaps with the traditional wheel strategy:

- sell puts

- accept assignment

- sell covered calls

However, modern NVDA trading often requires more flexibility.

This may include:

- active rolling

- synthetic adjustments

- spreads

- volatility-based sizing

- selective assignment management

Blindly running a mechanical wheel strategy on NVDA without volatility awareness can become extremely dangerous.

Realistic Performance Expectations

One of the biggest misconceptions around options selling is the idea of “consistent passive income.”

Reality is more complicated.

Premium-selling systems often experience:

- long periods of small gains

- occasional sharp drawdowns

- high emotional pressure during volatility spikes

Strong months can be followed by difficult periods.

There is no guaranteed monthly return.

Long-term success depends on:

- risk management

- adaptability

- avoiding catastrophic loss

- capital preservation

The objective is survival first.

Income generation comes second.

Who This Strategy Is NOT For

This framework is probably unsuitable for:

- traders seeking fast profits

- undercapitalized accounts

- inexperienced options traders

- traders uncomfortable owning NVDA shares

- traders unable to actively manage positions

- anyone relying on short-term option income to cover living expenses

Selling premium on high-volatility stocks requires active oversight and emotional discipline.

Frequently Asked Questions

Is selling puts on NVDA risky?

Yes. Extremely.

The primary danger comes from rapid downside moves, volatility expansion, and oversized exposure.

Are covered calls safe?

No.

Covered calls reduce downside slightly through premium collection but still expose traders to substantial equity risk if NVDA falls sharply.

Can the wheel strategy work on NVDA?

Yes, but only with disciplined sizing and active management.

Mechanical wheel strategies without volatility awareness can perform poorly during aggressive market moves.

What is the biggest risk when trading NVDA options?

Overleveraging.

Most catastrophic outcomes occur because traders deploy too much capital too aggressively.

Is NVDA better than other stocks for options selling?

NVDA offers:

- high liquidity

- elevated premium

- active weekly options

But those advantages exist because the stock is highly volatile.

Higher premium always comes with higher risk.

Final Thoughts

NVDA remains one of the most compelling option-selling environments in modern markets.

Its:

- liquidity

- volatility

- institutional participation

- weekly option structure

make it uniquely attractive for systematic premium strategies.

At the same time, it can punish poor risk management brutally.

The long-term objective should never be maximizing short-term premium.

The objective is building a repeatable framework capable of surviving:

- volatility shocks

- earnings gaps

- trend reversals

- prolonged market stress

Cash-secured puts, covered calls, and credit spreads are tools.

Risk management is the actual strategy.