The NVDA strategy didn’t start as a master plan. It emerged out of necessity.

About a year ago (2025), after the DeepSeek-related volatility shock that briefly crushed NVDA and other AI names, our stock portfolio was under pressure. I was using margin across multiple positions, volatility expanded fast, and I faced a margin call. That was the moment I decided to abandon complexity and build the entire portfolio around a single, highly liquid asset. I chose NVIDIA.

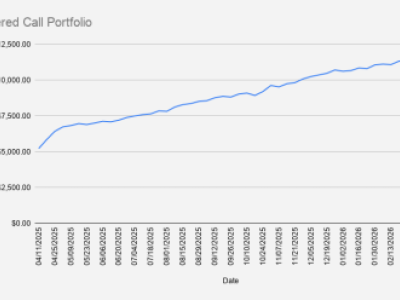

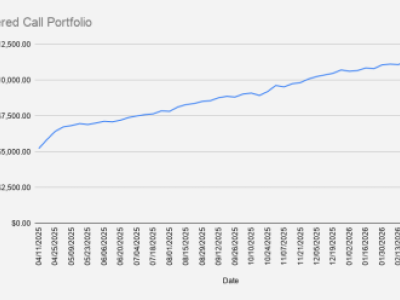

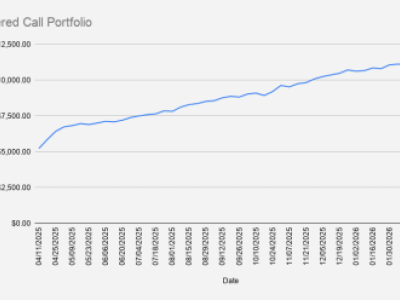

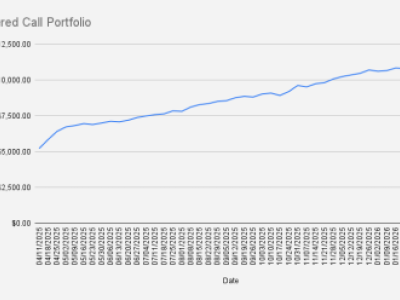

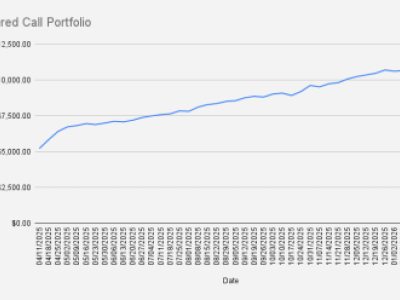

I bought 100 shares of NVDA on margin around the $110 level. Immediately after the trade, our account showed roughly –$6,700 in margin debt. From the start, this was not a “long and forget” position -it was a position that had to work, structurally.

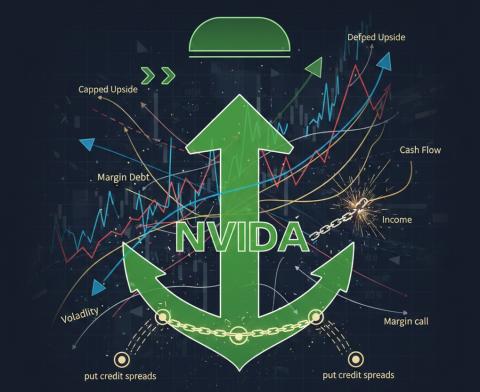

Very shortly after, NVDA did what it often does: it exploded higher. The stock ran from ~110 into the 160–170 range, then 180, and at one point traded above 220. However, because I began selling calls early - primarily to reduce margin stress - I had already capped most of the upside. That wasn’t an accident. It was the trade-off I consciously accepted in exchange for stability and cash flow.

From that point on, NVDA stopped being just a stock in the portfolio and became the portfolio itself.

Covered call writing turned into the core engine. Instead of trying to predict tops or chase breakouts, I focused on managing the position mechanically. When calls were challenged, I rolled them up and out. Over time, through repeated adjustments, my effective call level moved higher. As of now, after many rolls, it sits around 116.

To accelerate margin reduction and improve weekly cash flow, I added weekly put credit spreads, structured against the NVDA position. These spreads generate frequent, smaller premiums that help offset volatility and steadily reduce margin debt. Most weeks, premiums go straight toward stabilizing the account rather than opening new risk.

As a result, NVDA gradually took over the portfolio. For long stretches, it has represented 80% or more of total exposure. Occasionally, I allocate capital to other stocks, but those positions remain secondary. Concentration here is intentional: one asset, deeply understood, with tight control over risk and adjustments.

This is now the defining feature of my portfolio construction. NVDA is not just a trade - it’s the framework.

The strategy remains unchanged: stick with NVDA until margin debt is fully neutralized. Only once margin pressure is gone does freeing up upside make sense. Even then, that process will likely involve gradual rolling, not sudden removal of call coverage. The priority remains survival first, optionality second.

In other words, upside is deferred, not abandoned.

Potential Downsides and Risks

This approach is not risk-free, and it’s important to be explicit about that.

The most obvious downside is opportunity cost. NVDA’s massive upside moves have been partially or fully capped at various points. That’s the price paid for income and margin control.

There is also assignment risk. Selling weekly credit spreads introduces the possibility of being assigned additional shares. In a fast downside move, this could result in ending up long 200 shares instead of 100, increasing both exposure and margin usage at exactly the wrong time. While this risk is managed through sizing and strike selection, it cannot be eliminated.

Another risk is volatility regime change. If NVDA’s implied volatility compresses significantly while price stagnates, premium income will shrink, reducing the effectiveness of the strategy.

Finally, concentration itself is a risk. An NVDA-specific shock—regulatory, competitive, or macro—would disproportionately affect the portfolio.

This strategy is not designed to maximize returns in a straight line. It is designed to recover from leverage stress, generate income under volatility, and keep capital alive through extreme market conditions.

NVDA became the backbone of our portfolio not because it’s perfect, but because it allowed me to build a system that works under pressure. Until margin debt is gone and upside can be reclaimed safely, that system stays in place.