As of May 9, 2025, our covered call stock portfolio was valued at $6,818, reflecting another 1.42% week-over-week gain (+$95.42). Despite the recent uptick, we remain down -9.63% year-to-date.

Currently, the entire covered call portfolio is allocated to NVDA stock.

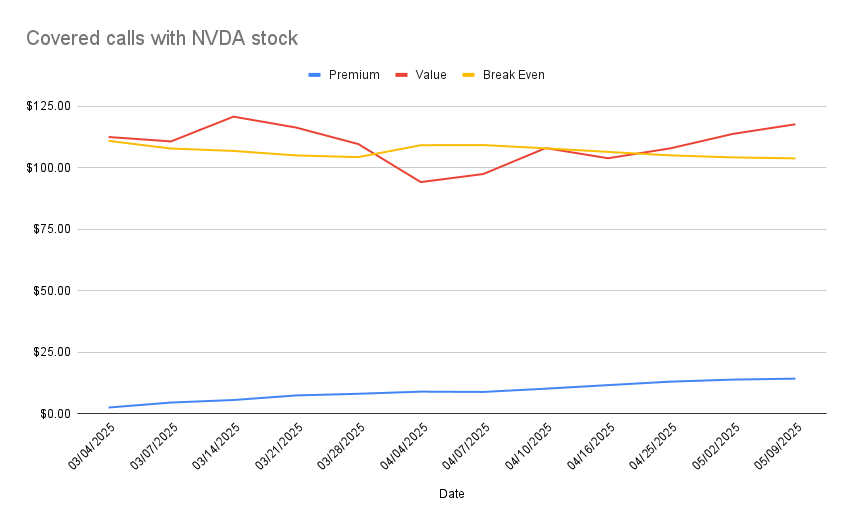

With NVDA rallying sharply, our May 9 $107 call moved deep in-the-money. Although my initial plan was to let the shares be called away and then re-enter via cash-secured puts, I decided to roll the position up and out for a net credit instead.

Unfortunately, weekly expiries offered unattractive premiums, so I rolled into the May 23 expiration:

- Bought back the May 9 $107 call for $10.62

- Sold the May 23 $108 call for $11.03

- Net premium collected: $0.41 per share

- Break-even price: $103.9

While the two-week premium of $41 may seem minimal—and only just covers my monthly margin interest—this roll allowed me to raise the strike price by $1. If NVDA closes above $108 on May 23, I will realize a total gain of approximately +$141 on the position.

The NVDA shares are currently financed through margin, with a total debit of -$6,320. The strategic goal is to generate sufficient options income over the next 12 months to fully own the NVDA position debt-free.

Assuming an average weekly premium of $20.50, it would take around 306 weeks (excluding interest) to pay off the margin balance. I aim to accelerate that timeline—but markets are unpredictable.

That said, the juicy premiums have dried up for now, and it's highly unlikely I'll reach my target of $500 in monthly options premium from NVDA this month. I'm fine with that—at least for now. The focus remains on long-term compounding and smart risk management, even if the short-term income dips.

If on the expiry date our strike prices are going to be deep in the money, I'm seriously considering switching to cash-secured puts

Subscribe to the Covered Calls newsletter to track every move, trade, and milestone as we work toward building a zero-debt, income-generating portfolio.